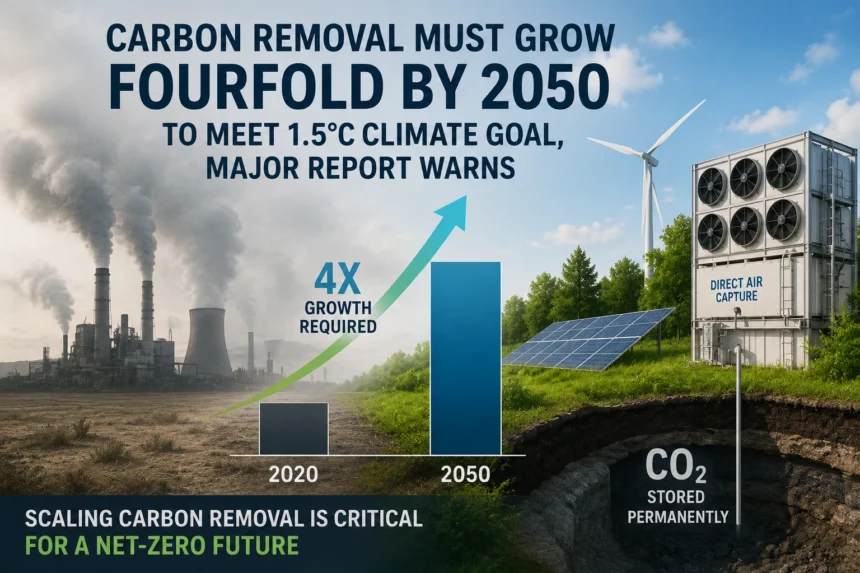

The world needs to remove carbon dioxide from the atmosphere nearly four times faster than it does today if it is to have any chance of limiting global warming to 1.5°C by the end of the century — and the window to build that capacity is closing fast.

That is the central warning of the third annual State of CDR report, authored by more than 50 scientists and released in 2026. The findings carry significant implications not just for global climate diplomacy, but for India’s own net-zero commitments and the role Indian companies must play in financing and deploying carbon removal technologies.

What Is Carbon Dioxide Removal — and Why Does It Matter?

Carbon dioxide removal (CDR) refers to deliberate human activities that pull CO₂ out of the atmosphere and store it — in forests, soils, the ocean, or underground geological formations. It is distinct from simply reducing emissions: CDR actively reverses what is already in the air.

Scientists consider CDR essential because emissions reductions alone are no longer sufficient to stay within 1.5°C. Global carbon output has already pushed the world onto what researchers call an “overshoot” trajectory — meaning temperatures are expected to breach 1.5°C in the coming decade before CDR can bring them back down.

The report defines three functions CDR must serve in the decades ahead: reducing net emissions in the near term, counterbalancing unavoidable residual emissions (such as methane from rice farming) in the medium term, and driving net-negative emissions in the long term to actually pull temperatures downward.

The Numbers: A Stark Gap Between Pledges and Reality

The world currently removes approximately 2.2 billion tonnes of CO₂ per year — roughly 5% of gross global emissions. Nearly all of this comes from conventional methods: tree planting, ecosystem restoration, and agroforestry.

To stay on a 1.5°C pathway, the report says global CDR must reach 8.75 billion tonnes per year by 2050 — a fourfold increase in under 25 years.

Current national climate pledges fall short by more than 5 billion tonnes per year by 2050. That gap has widened since the previous report, largely because the United States withdrew from the Paris Agreement and other major economies did not step up their ambitions in response.

The report models three scenarios:

- Current ambition (based on existing national pledges, excluding the US): CDR reaches 5.9 billion tonnes by 2050, with end-of-century warming between 1.7°C and 2.7°C. The world does not reach net-zero emissions under this path.

- Highest ambition (full global buy-in): CDR scales to 8.8 billion tonnes by 2050, temperatures peak around 1.7–1.8°C, and net-zero is achieved around mid-century.

- Delayed ambition (current targets until 2035, then maximum effort): CDR must reach 23.6 billion tonnes by 2100 — far more than the high-ambition path — because early inaction compounds the debt.

The takeaway is clear: delay is expensive. Every year of inadequate action requires far greater CDR effort later.

Conventional vs Novel: Where the Growth Must Come From

Today, 99.9% of all CDR is conventional — forests, soils, and land management. Novel technologies such as direct air capture (DAC), biochar, enhanced rock weathering, and bioenergy with carbon capture (BECCS) collectively remove just 2 million tonnes per year — a fraction of a fraction.

The good news: novel CDR has been growing at roughly 40% per year, a rate comparable to early solar energy adoption. The bad news: even at that pace, it is nowhere near sufficient.

The report notes that conventional methods, while necessary, come with limitations. Forest-based removal is vulnerable to fires, drought, and land-use pressure. Novel methods offer more durable, verifiable storage — but at significantly higher cost.

Cost ranges vary enormously by method:

- Forestry-based CDR: as low as $5–$53 per tonne of CO₂

- Soil carbon sequestration: up to $150 per tonne, though sometimes cost-neutral when crop yield improvements are factored in

- Direct air carbon capture (DACCS): among the most expensive options currently available

The cheapest methods tend to offer less permanence; the most durable tend to be the most expensive. Scaling both simultaneously is the challenge facing governments and investors.

Funding Has Grown — But Unevenly

Total grant funding for CDR research has reached approximately $5.6 billion since 2005, with around one-third of that committed in the past three years alone. Investment in CDR companies also recovered in 2025 after a brief dip, now representing about 3% of all climate-tech funding.

Yet the report describes the innovation ecosystem as “uneven” and cautions that there is “no strong evidence of a step-change.” CDR patent activity actually peaked in 2011 and has declined since. Pilot projects are concentrated in a handful of countries — primarily Sweden, Denmark, and the United States.

The voluntary carbon market, which drives most current demand for novel CDR, contracted for just 0.04 billion tonnes of removals last year. A significant share of purchases came from a single buyer — Microsoft — which the report flags as a “critical vulnerability.”

Policy: Progress in Some Places, Reversal in Others

Of the G20 nations, policy support for CDR remains patchy. The European Union is the only jurisdiction to have enshrined a binding, quantified removals target into law. The UK and Australia have set specific goals for scaling novel CDR over the coming decade. Canada, Germany, and Switzerland are taking proactive steps through financial support and integration with emissions trading systems.

The US, which the report previously described as a global leader on CDR, has reversed course under the Trump administration, freezing or dismantling funding and support programmes.

Most CDR policy globally focuses on supply — building capacity — rather than demand. The report argues this is a structural problem: CDR has no natural market. Without policies that create buyers, scale-up will stall regardless of how much capacity exists.

What This Means for India

India is not among the top contributors to CDR today, though it features as a significant forest carbon country. The report identifies China, the United States, the EU, Brazil, and Russia as the largest contributors to current removals.

But India’s relevance to this story is growing rapidly.

India’s net-zero target of 2070 implies a substantial role for CDR in the second half of the century, particularly as hard-to-abate sectors — steel, cement, agriculture — will generate residual emissions long after the grid is clean.

SEBI’s BRSR framework already requires India’s top 1,000 listed companies to disclose their sustainability performance, including emissions. As global pressure for Scope 3 accounting and supply chain decarbonisation intensifies, Indian companies exporting to the EU, UK, or US will face growing scrutiny of their carbon strategies — including whether they are investing in credible removal solutions.

India’s domestic market for CDR is nascent, but the ingredients are present: large land areas suitable for reforestation and soil carbon, agricultural residues usable for biochar, and a growing green finance ecosystem. What is missing is policy intent, investment frameworks, and awareness in the corporate sector.

The Bottom Line

The third State of CDR report is both a progress update and an alarm. Carbon removal is no longer a fringe concept — it is a mathematical necessity for any credible 1.5°C pathway. The technologies exist. The science is maturing. The funding is growing, if unevenly.

What is still missing, globally and in India, is the policy architecture and corporate urgency to treat CDR as the strategic priority it has become.

The report’s most sobering finding may be its simplest: the period 2026 to 2030 is crucial. The decisions made in these four years — by governments, investors, and companies — will largely determine whether CDR can fulfil its role in the decades that follow.

Sources: Edwards et al. (2026), State of CDR Report — Third Edition. Coverage informed by Carbon Brief analysis.

ESG World News covers sustainability, climate policy, and corporate ESG developments across India and the world. For more on India’s BRSR framework and net-zero commitments, explore our India Focus section.